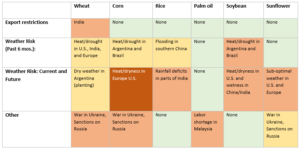

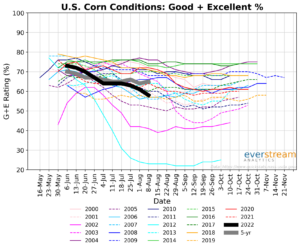

Both France and Romania, Europe’s top two corn producers, have suffered unprecedented heat and dryness in July. As these conditions are likely to continue into August, EU annual crop output will register well below average volumes. Extreme heat is lowering water levels on the Rhine River, vital for agricultural transport. Water depletion is likely to continue throughout August, ultimately dropping so significantly that vital transport operations will be halted.

Sunflower

The China-bound Star Helena, carrying a cargo of 45,000 tons of sunflower meal, was among the first vessels to depart Ukraine following the signing of the agricultural export deal with Russia. Shortly thereafter, the Italy-bound Mustafa Necati vessel departed, carrying another 6,000 tons of sunflower oil. Despite this positive development, Ukraine’s sunflower meal exports are forecast to decline from 66% to 40% of the global share. Similarly, its sunflower oil exports are forecast to plunge from 50% to 35% of the global share.

Palm oil

From August 1, Indonesia has increased the permitted palm oil export volumes to 9x domestic sales, up from the 7x that was previously established. Meanwhile in Malaysia, daily losses of palm oil fruit are still estimated at 57,880 tons due to an acute shortage of plantation labor. The labor crunch was further complicated in mid-July when Indonesia suspended sending its citizens to work in Malaysia over a breach in a worker recruitment deal. Though the suspension was lifted on August 1, the palm oil industry in Malaysia is still 120,000 workers short of what is needed to reach and maintain desired production levels. Despite the production challenges in Malaysia, the stockpile of palm oil fruit in Indonesia is expected to lead to a further decrease in global palm oil market prices.

Rice

Seasonal monsoon rainfall deficits in India, the world’s largest rice exporter, has caused a decrease in rice cultivation estimated at 13%. India’s top rice-producing states of Bihar, West Bengal, and Uttar Pradesh, together contribute about one-third of the country’s annual rice production volumes. Across the rice acreage within these areas, summer monsoon rainfall through early August has only registered 75% of normal which also ranks as the fifth lowest of the past 30 years. Compared to last year, rice production could fall by up to 8%, or 10 million tons. The certainty of a lower output is prompting concerns that the Indian government may impose export curbs in response to rising prices. Production success will be dependent on the reliability and consistency of future monsoon rains.

Sugar

On August 5, India announced that it will allow sugar mills to export an additional 1.2 million tons for the current marketing year running through September. This is in addition to the previous cap of 10 million tons, after which it became clear that raw sugar stockpiles in ports and warehouses were quickly exceeding capacity. A variable monsoon rainfall pattern across central and northern India has complicated transport logistics from sugar mills to ports, potentially delaying exports. In the next two months, authorities will decide if an export cap on sugar will be implemented for the 2022-2023 season which begins in October. The speculated cap is between 7-8 million tons.

Outlook and recommendations: Key developments to monitor this summer

Though measured progress has been made on the geopolitical front, continued extreme weather throughout August will complicate the global food supply. Heat waves and drought persist across the Americas and Europe. Meanwhile, concurrent risks from localized flooding in parts of China and India add to the possibility of inadequate yields and lower production. Though the resumption of agricultural exports from Ukraine provides hope for global wheat and grains supply, success will depend largely on Russia’s willingness to cease disrupting port operations. The Odesa port bombing indicates that success is not guaranteed, and progress is quickly reversible. Until guarantees can be made, it is likely that shippers will avoid such export routes.

Everstream clients are receiving detailed information about this disruption.

Contact us to learn how we can give you a complete view of the risks affecting your end-to-end supply chain and what you can do to mitigate them.