Energy prices across Europe are reaching all-time highs as ongoing disruptions to pipeline flows and a scorching summer season continue to take their toll on gas supplies. In response to these developments, the European Union has been drafting intervention plans in its energy market in the short term, seeking to rein in soaring power costs and breaking the link between gas and electricity prices. One proposal included capping prices of natural gas used for power generation.

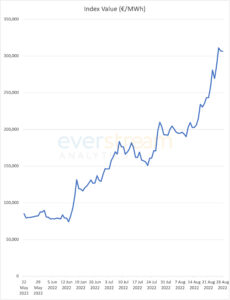

Figure 1: Snapshot of TTF neutral gas price index (source: European Energy Exchange).

Year-ahead rates for German gas has steadily climbed above €1000/MWh ($1000/MWh) as uncertainty continues to mount over another maintenance closure of the Nord Stream 1 pipeline that is scheduled to last from August 31 until September 2. Gazprom has claimed that gas flows should return to 20% of pipeline capacity following the maintenance shutdown which is allegedly required for works on the pipeline’s compressor. This explanation has been rejected by European authorities as a pretext for Russia to increase pressure on the continent’s energy supplies and future deliveries via the pipeline continue to remain dependent on developments in EU-Russia relations

The halt in Nord Stream flows will place further stress on Germany’s struggling energy providers which are now waiting for an October 1 levy on natural gas to come into effect. The €0.02419/kWh (€24.19/MWh) gas levy was announced on August 15 and is being introduced by Germany’s nationwide gas trading hub, Trading Hub Europe GmbH. The gas levy is intended to help struggling energy providers including Uniper SE and SEFE Marketing & Trading (formerly Gazprom Germania) avoid bankruptcy. The levy will remain in effect from October 2022 until April 2024 and will apply to all end users including households and industrial users.

In addition to Germany, rising energy costs across the continent have also been worsened by disruptions to alternative fuel supplies including nuclear power, coal, and oil. For example, year-ahead rates for natural gas in France have soared past €1,100/MWh ($1,100/MWh) as state energy operator Électricité de France S.A. continues to struggle with repair and maintenance works that have put over half of the country’s 56 nuclear reactors out of commission and turned the nation into an energy importer. Russian oil deliveries to the Czech Republic, Slovakia, and Hungary via the Druzbha pipeline were also briefly disrupted from August 4 until August 12 due to a payments dispute while coal and oil deliveries to plants along the Rhine River were disrupted for much of the month by historically low water levels that have only just begun to recover.

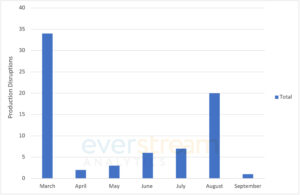

Production disruptions

Manufacturers across the continent continue to struggle with insufficient supplies and rising energy costs, with data from Everstream Analytics revealing that the number of energy-related production disruptions across the continent are now at their highest level since the beginning of the Russia-Ukraine conflict. As in previous months, German companies continue to remain most exposed to the ongoing energy crisis, with industry groups warning that the planned gas levy could place even more pressure on struggling manufacturers.

Figure 2: Number of energy-related factory disruptions in Europe by month (source: Everstream Analytics).

Warnings have been issued by the German Chemicals Industry Association (VCI), which has indicated that chemical firms in the country can only replace around 2-3 TWh of production with oil and coal out of the nearly 135 TWh of energy that the industry obtains from gas yearly.

Other German manufacturers that depend heavily on natural gas supplies are at risk of production cuts as rising natural gas prices have made it more expensive to operate glass making furnaces. The German Association of the Automotive Industry (VDA) has also signalled that transitioning away from natural gas would be difficult for the industry as any long-term modifications to the production process would likely impact output and increase the industry’s power demand by up to 15%.

Ammonia and nitrogen fertilizer manufacturers across the continent also continue to be affected by rising energy prices, with chemicals and fertilizer manufacturers slashing output and halting production.

In addition to chemicals companies, an official from Italy’s Ecological Transition Ministry also revealed on August 21 that Italian manufacturers in the glassmaking and canning industries have also been forced to scale back production in the face of rising energy costs. Spikes in energy prices have also affected smaller EU economies including Lithuania, Estonia, and Latvia.

Gas storage fill levels pick up speed in parts of Europe as winter approaches

Gas storage levels across the continent have continued to rise at a steady pace, with storage levels in Croatia and Belgium rising by 11% and 8.54%, respectively. Storage levels in Germany continue to increase faster than planned and are currently on track to reach 85% storage capacity by the beginning of September, one month ahead of schedule. Latvia, Austria, and Hungary remain at high risk of gas supply disruptions during the coming winter, and all imported at least 80% of their natural gas supply from Russia in 2021. The fill rate of all three countries remains well below the EU average of 80%, with Latvia’s being the lowest at 55%.

Everstream clients are receiving more detailed insights and recommendations about this risk.

Contact us to learn how we can give you a complete view of the risks affecting your end-to-end supply chain and what you can do to mitigate them.